The increasing popularity of online banking is nothing new. So-called challenger banks / neobanks are giving traditional banks a run for their money. While old-school banks still have their place, some reports predict that mobile-only banks are set to overtake visits to high street banks in just a few years.

It’s easy to see why consumers might opt for banking apps. After all, transactions can be completed on-the-go, from anywhere, across different currencies, usually at cheaper rates than traditional banks.

In light of that, we’re taking a look at two such challenger banks: N26 and Monzo. Both are virtually unknown in the United States but very active in Europe. However, in the case of N26, it shut down its British operation in 2020.

Please also note that neither N26 nor Monzo offers credit cards. That's enough preamble- there’s a lot to tell you about, so let’s make a start.

What is N26?

This Berlin-based bank has been around since 2013. With 5+ million customers based in over 25 countries, it’s grown to employ as many as 1,500+ staff.

N26 is keen to advertise its commitment to banking transparency. New customers can spend as soon as their account's open – before they even receive their debit card!

At this point, it's worth noting that US citizens can access some but not all of N26’s features. However, as stated in the intro, as both N26 and Monzo are EU-based and EU-focussed, that’s what we're focusing on.

👉 Read our N26 review for more info.

What is Monzo?

Like N26, Monzo is one of the earlier tranches of app-based digital banks. Based in the UK, it was established in 2015 and also employs around 1,600+ people. It boasts almost 5 million customers and advertises its services as “banking that makes a statement.”

Similar to N26, Monzo is keen to emphasize its commitment to transparency, stating: ”We're building a bank, together. By solving your problems, treating you fairly, and being totally transparent, we believe we can make banking better.”

Monzo’s head office is in London, and like N26, it is primarily aimed at EU citizens. It does, however, like N26, offer some services in the US.

N26 vs Monzo: Their Pros and Cons

We’ve covered a lot of detail, so let’s take it back to a simpler comparison with a quick pro-cons list. Here are the advantages and disadvantages of both N26 and Monzo at a glance:

N26’s Pros 👍

- Free standard delivery for card shipments

- Free accounts and cards are available

- N26 ‘spaces’ are great for budgeting

- There’s a desktop version with dark mode available for convenient online banking

- N26 has a full banking license

N26’s Cons 👎

- N26 provides limited services within the US

- N26 doesn’t operate in the UK

- Withdrawals abroad are charged a 1.7% transaction fee

- You won’t accumulate any interest on your savings

Monzo’s Pros 👍

- You get access to a convenient app that comes with plenty of tools to help you budget, save, and manage your money (available both on Android and iOS)

- Monzo is a real bank registered with the FCA

- You can earn interest on funds as you save

- You can set up joint accounts

- It's easy to create direct debits

Monzo’s Cons 👎

- There are saving rates, but these aren’t the most attractive on the market

- Travel money is charged at Mastercard’s exchange rates instead of interbank’s, which can work out more expensive compared to its competitors

- Every time you want to deposit money into your account, you’re charged £1

- A 3% charge is applied to withdrawals abroad when you exceed your monthly limit.

- There isn’t a desktop app available.

N26 vs Monzo: Their Core Features Compared

It’s important to consider not just your current digital banking needs but what they may also be in the future. So, be sure to bear that in mind as we explore N26 and Monzo’s core features for personal and business customers:

N26

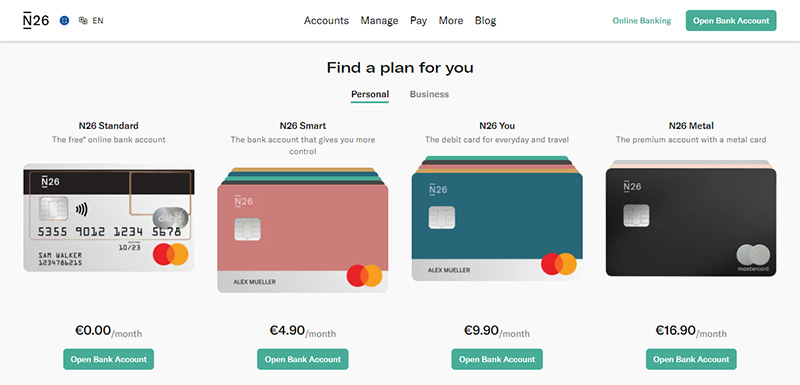

Customers can open either a personal or business account. First off, let’s take a look at the personal accounts, of which there are four types (we'll cover their fees further down):

Standard: This is N26’s free account and comes with limited features. Customers can make contactless mobile payments with Google and Apple Pay. The N26 Mastercard debit card issued to customers is transparent, free, and can be used worldwide. You can also impose spending limits, make free payments, and you get three free monthly ATM withdrawals within the Eurozone.

Smart: This account comes with all the Standard features, plus you can order an additional debit card for free in a range of colors (aqua, ocean, rhubarb, or slate) – the choice is yours! Also, the number of free monthly ATM withdrawals you can make within the Eurozone rises to five.

You: In addition to the features you’ve just read about, you have the bonus of being able to make unlimited withdrawals in any foreign currency within the Eurozone.

Metal: This is N26’s premium account (and therefore, its most expensive!), and for some added glamour, customers receive an 18-gram metal Mastercard debit card.

We’ve also summarized N26‘s key features that we think you’ll be interested in:

Money Management

N26 customers can launch sub-accounts (which effectively double-up as savings accounts) called “Spaces.” Their purpose is to make it easier to track your money and manage your spending. You can set savings targets and make regular payments into them – once you've set these up, N26 does the rest automatically.

Customers can also access what N26 calls “Shared Spaces.” Here, if your friends/family have N26 accounts, you can save towards similar goals.

Each of the personal accounts listed above receives 10 “Spaces” apart from the free Standard Account, which only offers customers two.

Making Payments

N26 seamlessly integrates with MoneyBeam so that customers can receive and send money with ease.

Customers can also use Apple Pay and Google Pay to make payments.

Or, if you're moving money overseas, N26 integrates with Transferwise (read our Transferwise review). This enables you to transfer money into 38 different currencies at cheaper rates than old-school banks.

Lastly, you can also receive incoming payments via SEPA instant credit transfer.

Reports and Statistics

N26 uses AI to categorize your spending automatically. All personal account holders get monthly reports on how you're managing money across the different spending categories. This also provides a general overview of all your inbound and outbound transactions.

N26 Business Accounts

Now, let’s zone in on N26’s business accounts – these are great for startups. Like their personal accounts, there are four to choose from. Again, there are fees, but we'll cover those lower down:

Business: This account is free, and with it, you can make mobile and contactless payments with Apple Pay and Google Pay. Customers receive a debit Mastercard and 0.1% cash back on card purchases. Worldwide payments are free, and you can make three free ATM withdrawals within the Eurozone.

Business Smart: This is a paid-for account. Customers receive the same benefits as the free account and an optional free colored Mastercard debit card (same colors as the personal account offer). You can also withdraw money five times a month from an ATM for free within the Eurozone.

Business You: You get everything in Business Smart, with the same ATM withdrawal limit. However, the smart account unlocks unlimited free withdrawals in any currency.

Business Metal: This is N26's most extensive business account, and as such, it’s the most expensive. Here, you'll get an 18-gram metal card, for which you can also receive 0.5% cashback. Lastly, you can make up to eight free monthly ATM withdrawals within the Eurozone.

N26’s business accounts also include the following capabilities:

Managing Your Money

Like personal account customers, business account holders are allocated “Spaces.”On top of that, business account customers (apart from those on the free plan) can access N26’s “Round-Up” feature.

Here, all your card transactions are rounded up to the nearest Euro, and the price difference is automatically transferred to a “space” so you can save more easily. Account-holders can also track all their financial transactions, including invoice payments, and download them into CSV or PDF formats for tax return purposes.

Other Perks

In addition to the banking features we’ve just outlined, N26 likes to give its customers good value for money. Below is a list of other features this online bank offers paid-for customers.

What you’re entitled to will depend on the pricing tier you’ve opted for. We aren’t covering those in this review. Still, they may be relevant, especially if you’re a frequent traveler and/or looking for insurance. Here are a few examples of the extras on offer:

- Mobile phone insurance

- Mobility insurance for vehicle rentals

- Travel insurance

- Travel health insurance including baggage delays, emergency medical insurance, flight delays, and trip cancellation.

Monzo

Like N26, Monzo splits its banking offer into personal and business accounts. Let’s check out the personal accounts first. There are three to choose from, including a freemium package (again, we’ll list pricing lower down in this review):

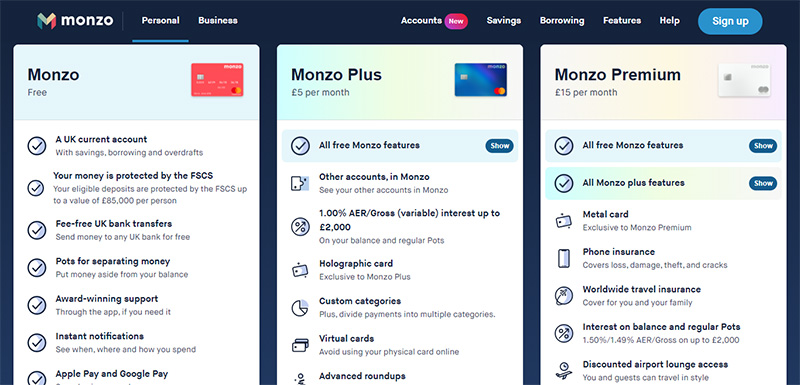

Monzo Current: This is Monzo’s free current account and comes with a free debit Mastercard. Here, you get access to lending, overdrafts, and savings. You also benefit from deposit protection from the Financial Services Compensation Scheme (FSCS) up to the value of £85,000 per person.

Account-holders can make bank transfers to any UK bank account for free. You’ll receive real-time notifications regarding spending; you can make contactless payments and use Apple Pay and Google Pay for mobile transactions. There’s no minimum term for which you have to hold this account.

Monzo Plus: This mid-range account has a minimum term of three months. Aside from all the features included in the basic Monzo Current Account, you also get a free holographic debit Mastercard. On top of that, you'll also get:

- 1.00% AER/Gross (variable) interest on balances up to £2,000 and on regular deposits in your “Pots” (see below).

- You can withdraw up to £400 abroad with no fee every 30 days.

- One free cash deposit per month in the UK.

- A free “virtual” card – you can have up to five virtual cards in different colors.

Monzo Premium: This is Monzo’s most expensive account, and on top of the features listed above, customers also receive a metal-colored debit Mastercard, phone and travel insurance, discounted airport lounge access, 1.5% interest AER/Gross (variable) on balances of up to 32,000 and on regular “Pot” deposits.” You also benefit from up to £600 fee-free withdrawal overseas every 30 days and five free cash deposits a month in the UK. This account must be held for a minimum of six months.

Monzo also offers a Monzo Joint Account and a Monzo 16-17 Account.

Aside from the above features, Monzo also offers the following capabilities:

Money Management

All personal account holders receive instant notifications that enable them to track where they’re spending and how much. Like N26 account holders, spending is also automatically categorized, so it’s easier to track.

Similar to N26’s “Spaces,” Monzo gives customers the option of putting money aside into “Pots.”

Customers can divide their payments into different categories with personalized budgeting. You’ll be able to create custom categories and even divide single transactions into multiple categories.

Monzo Plus and Monzo Premium customers can also:

- Auto-export their transactions into Google Sheets

- Track how their credit score changes

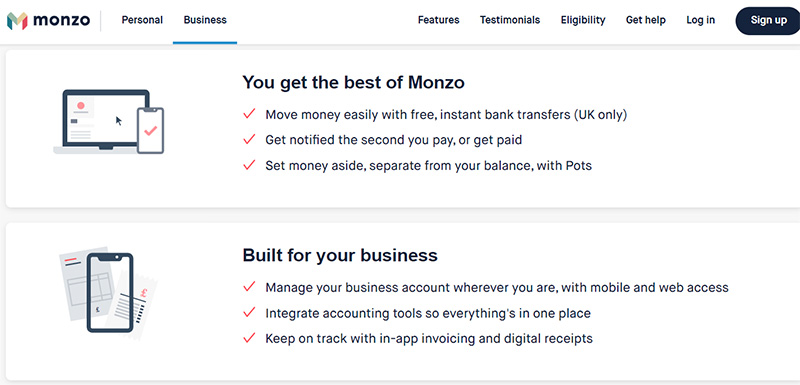

Monzo’s Business Accounts

Now let’s zone in on Monzo’s business accounts. Unlike N26’s business accounts, there are just two options:

Monzo Lite: This is Monzo’s free business account, and with it, customers receive a full UK current account. Plus, you can:

- Make payments using Apple and Google Pay

- Full mobile and web banking signup

- Account switching if you’re moving from another bank

- Fee-free spending overseas

- You can manage your scheduled payments

- Access to advanced security features

- You can pay in cheques and cash for free

- A pebble or slate grey business debit card

- Free and instant money transfers to UK banks

- Digital receipts

- Instant notifications

- Pots (the same as personal account customers receive)

Monzo Pro: As well as all the features listed above, you can create, send and track invoices and set aside money in “tax pots” for when it’s tax return time. You can also integrate with accounting software, including Xero, QuickBooks, and FreeAgent. You also get free access to Xero for the first six months, up to two account users for Ltd companies, as well as exclusive offers.

N26 vs Monzo: Their Costs

We’ve already talked about what accounts are available with N26 and Monzo. Now it’s time to dive into how much these will set you back:

N26

- The Standard plan and Business plan is free.

- The N26 Smart and Business Smart plan costs €4.90/month.

- N26 YOU and Business You package costs €9.90 per month.

- N26 Metal and Business Meta programs costs €16.90 a month.

N26 offers free standard delivery with your first card after opening an account or upgrading. If you want express delivery (which takes up to 3 working days), there’s an additional €20 fee.

Also, if you go over your free ATM withdrawal allowance, you’re charged €2, on top of the 1.7% transaction fee.

Monzo

Monzo Current and Monzo Lite are available for free. These are the basic personal and business cards, but you can only withdraw up to £200 abroad for free before being charged a 3% fee on your withdrawals. You’re also charged £1 when you deposit into your account via one of the 28,000 PayPoint’s located across the UK.

Monzo Pro and Monzo Business Pro: This account costs £5 per month, but you don’t pay fees for withdrawals abroad up to £400. You also get one free UK cash deposit. However, this account requires you to sign up for a minimum of three months.

Monzo Premium: This account will set you back £15 per month. You don’t pay fees on international withdrawals up to £600. You also get five free cash deposits at PayPoint’s across the UK. However, you’ll have to sign up for a minimum of six months.

Shipping your Monzo card is free within the UK and costs £30 for international delivery.

N26 vs Monzo: Customer Support

When money is part of the conversation, there can be no uncertainties. So, how well equipped are N26 and Monzo when it comes to handling your questions and concerns?

N26

You can contact N26 25/7 via live chat on their website or within the app. With a premium account, telephone support also becomes available, and if you have a metal card, you get access to priority support on a dedicated hotline.

Or, if you prefer to go down the self-help route, N26 has an online help center where you’ll find the answers to their most frequently asked questions.

Monzo

Monzo also provides an online help center with self-help resources split up into categories like emergencies, your account, mobile payments, pots and budgeting, overdrafts, etc.

Alternatively, you can contact Monzo’s support team in-app via live chat or on the phone. Live chat is available 24/7!

N26 vs Monzo: Our Final Verdict

N26 and Monzo provide convenient services for those who want to budget and save their money via their smartphones’ convenience.

That said, overall, N26 is the cheaper travel card with smaller transaction fees on withdrawals abroad. They also provide a desktop app, which might appeal to more traditional bank users who want banking flexibility with both their smartphones and desktops.

On the other hand, Monzo has the edge where offering joint accounts and interest on your savings are concerned. That said, their foreign withdrawal rates aren’t as cheap.

Lastly, your location is another huge factor to consider. Monzo serves UK citizens, whereas the UK isn’t covered by N26 at all. N26, on the other hand, is incredibly popular throughout the rest of Europe.

Now we’re at the end of this review, tell us which side of the N26 vs Monzo debate you fall on in the comments below! Or, are you considering one of their competitors like Revolut, Starling Bank, or Monese? Either way, tell us all about it – we look forward to hearing from you soon!

Comments 0 Responses